About 70% of homeowners who go solar today use some form of zero-down financing — no upfront payment, panels on the roof, and electricity bills that (supposedly) drop from day one. That pitch is compelling, but the fine print matters enormously. Whether you come out ahead depends on which product you choose, your electricity rate, how long you stay in the home, and whether you qualify for the federal tax credit. The wrong financing choice can cost you tens of thousands of dollars over the life of a system.

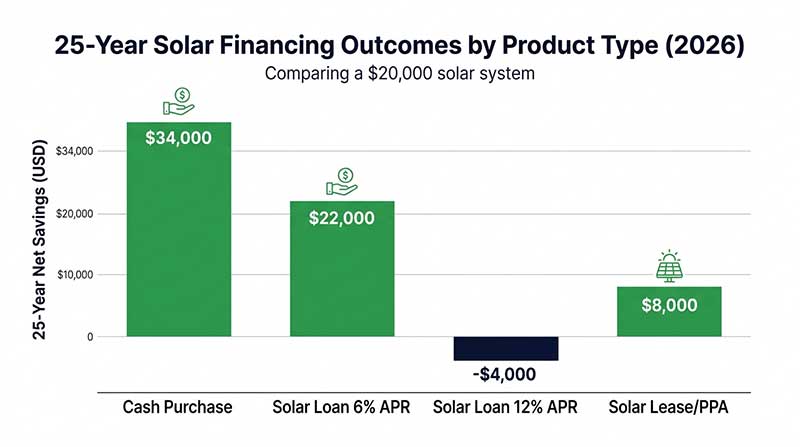

Zero-down solar broadly covers three products: solar loans, solar leases, and power purchase agreements (PPAs). All three let you avoid the $15,000–$30,000 upfront cost of a cash purchase, but they work in fundamentally different ways. A solar loan gives you ownership; a lease or PPA does not. That ownership distinction drives almost every other difference — from tax credits to home resale value to what happens if you want to sell your house in year six.

This guide walks through each financing type with real numbers, explains the scenarios where zero-down solar genuinely makes sense, and flags the situations where you’d be better off saving up or choosing a different product entirely.