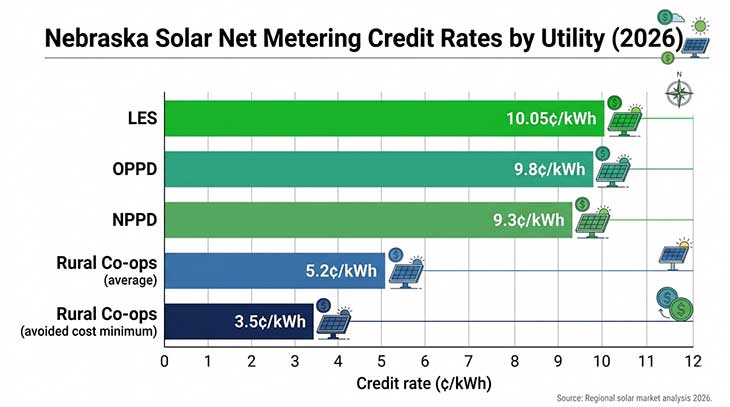

Nebraska has more than 330 sunny days of solar potential each year, yet ranks near the bottom nationally for installed solar capacity — and the main reason is the state’s unusual utility structure, not the weather. Unlike most US states where investor-owned utilities dominate, Nebraska is the only state in the country that relies entirely on publicly owned utilities: the Nebraska Public Power District (NPPD), Lincoln Electric System (LES), Omaha Public Power District (OPPD), and a patchwork of roughly 30 rural electric cooperatives. Each of those entities sets its own interconnection rules, net metering rates, and export compensation policies, which means what your neighbor gets for excess solar energy depends almost entirely on which utility serves your address.

That fragmented structure creates real complications for homeowners trying to model a solar investment. A system that pays back in 9 years under LES in Lincoln might take 14 years or longer under a rural co-op that pays avoided-cost wholesale rates instead of retail. According to SEIA data, Nebraska had only about 98 megawatts of installed residential solar as of late 2025 — a fraction of what comparably sunny Kansas or South Dakota have achieved. Understanding why requires a closer look at each major utility and the specific policy guardrails they impose.

This guide focuses on the three largest systems — NPPD, LES, and the rural co-op network — and explains exactly what the rules mean for your solar economics. Numbers matter here, so every figure below is tied to a published tariff or official rate schedule.