The average residential solar system in the United States costs $30,505 before incentives — and with the federal residential solar tax credit (Section 25D) having expired on December 31, 2025, how you finance that system now matters more than ever. A poorly structured solar loan can add $5,000 to $8,000 to your total cost through hidden dealer fees alone, wiping out years of electricity savings. The good news is that the range of financing options has never been wider, and borrowers who understand the landscape can still lock in competitive rates well below 8% APR.

Solar loans remain the most common path to ownership in 2026, used by roughly 31% of new residential solar customers according to SEIA data. Unlike leases or power purchase agreements, a loan lets you own the system outright and claim any state tax incentives or utility rebates that may still be available in your area. The trade-off is that you carry the full cost of the system on your personal balance sheet — which is why choosing the right loan structure is a decision worth spending real time on. Before you sign anything, use a solar loan calculator to model different rate and term combinations against your projected electricity savings.

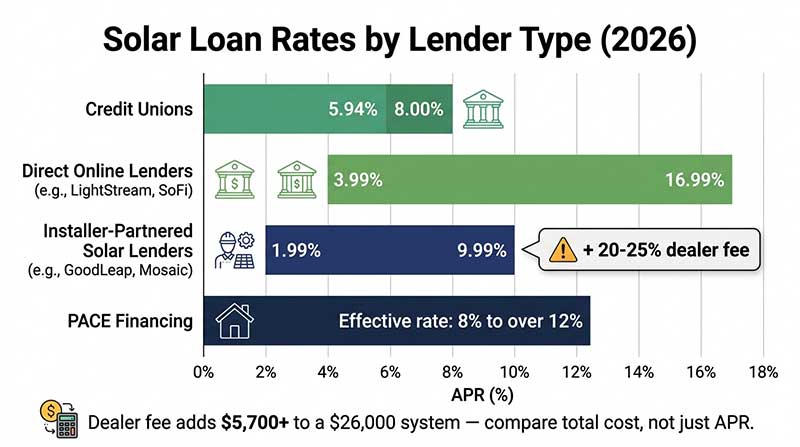

This guide covers the main lender categories available in 2026, the rates you should realistically expect, the hidden fee structure that catches most homeowners off guard, and the alternatives — particularly HELOCs and credit union loans — that often beat advertised solar loan rates on total cost.