What Net Metering Policy Changes Mean for Your Solar Decision

If you are evaluating solar in 2026, the trajectory of net metering policy in your state matters almost as much as the current rules, because most solar systems operate for 25–30 years and the policy environment will almost certainly evolve during that window.

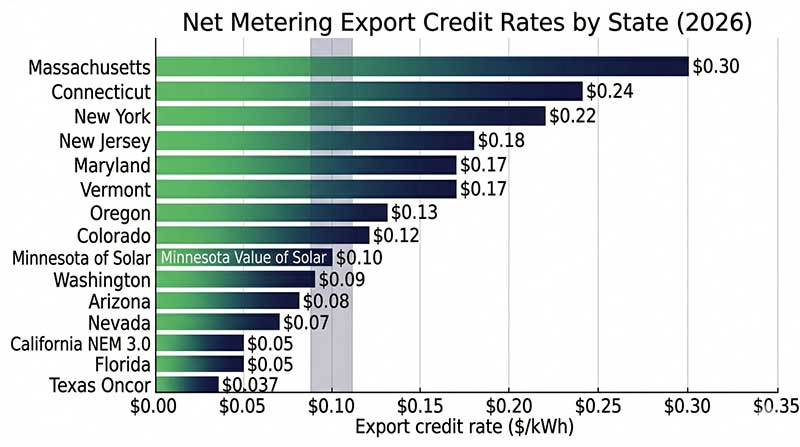

The general direction nationally has been toward lower export credits and cost-of-service reforms driven by utility arguments about fixed-cost recovery and grid infrastructure maintenance. The Edison Electric Institute, which represents investor-owned utilities, has argued in PUC proceedings across multiple states that retail-rate net metering creates a cost shift onto non-solar customers of $1–3 billion per year nationally. Solar advocates contest both the methodology and magnitude of those figures, but the regulatory and legislative trend since 2020 has clearly moved toward rate structure reforms in larger states, particularly those with higher solar penetration rates above 5% of retail load.

That said, the pace of change varies enormously. States with strong solar advocacy organizations and favorable legislative climates — New York, New Jersey, Oregon, Colorado, and Illinois — have successfully blocked or delayed utility-backed reform proposals. States with weaker consumer protection frameworks or utility-friendly commissions — Georgia, Arizona post-2017, and parts of the Southeast — have moved faster toward reduced credits.

Illinois is a notable recent example moving in the opposite direction: the 2021 Climate and Equitable Jobs Act locked in full retail-rate net metering for new residential customers and added a credit adder for low-income solar installations. Illinois retail rates averaging around $0.14/kWh in 2026 make it a strong policy environment for new solar through at least the late 2020s.

If you are in a state with a grandfathering provision — California, Florida, and Nevada all have versions of this — and the window for grandfather eligibility is still open, there is a meaningful financial argument for moving quickly. Grandfathered customers in California under NEM 2.0 are estimated to receive $5,000–$8,000 more in lifetime bill savings than equivalent systems installed under NEM 3.0, according to analysis by the California Solar and Storage Association. EIA projects retail electricity rates will increase nationally by an average of 2–3% per year through 2030, which improves solar economics over time but does not offset the impact of a major net metering restructuring for new customers.

Before committing to a contract, use a solar ROI calculator that inputs your state’s specific credit rate, local retail rate, and a conservative future rate escalation scenario — it is the most reliable way to judge whether the economics work under your current state policy before signing anything.