The federal solar tax credit is worth 30% of your total solar installation cost — and for the average American homeowner who spent around $29,000 on a rooftop system in 2025, that translates to roughly $8,700 back on their federal tax bill. Yet a surprising number of people either miss the credit entirely or fill out IRS Form 5695 incorrectly and leave money on the table. This guide walks you through every line of the form so you can claim what you’re owed.

The credit is officially called the Residential Clean Energy Credit, and it applies to solar panels, battery storage systems, and qualifying solar water heaters. The IRS extended the 30% rate through 2032, after which it steps down to 26% in 2033 and 22% in 2034 before expiring for residential installations. If you installed your system in 2024 or 2025 and haven’t claimed the credit yet, now is the right time to get Form 5695 right.

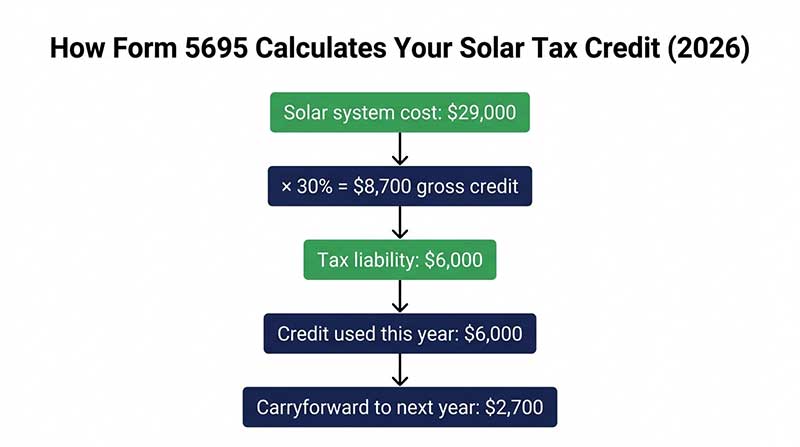

One important clarification: the solar tax credit is a nonrefundable credit, not a rebate. It reduces the federal income tax you owe, dollar for dollar. If your credit exceeds your tax liability in a given year, you don’t get a check for the difference — but you can carry the unused portion forward to the following tax year. Understanding that distinction before you fill out a single line will save you considerable confusion.