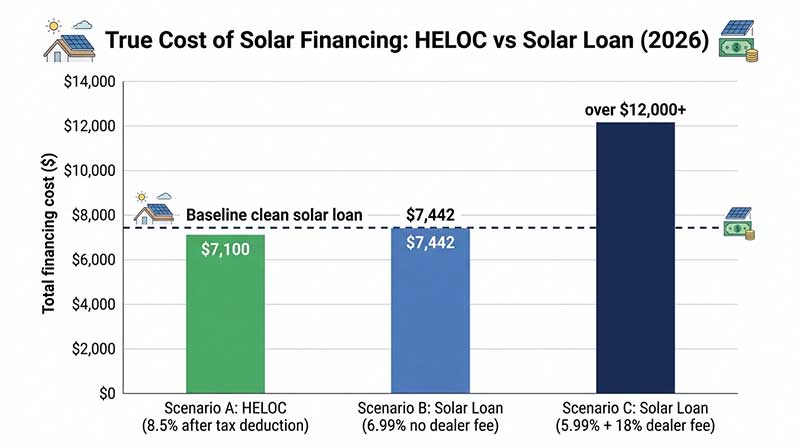

The average American homeowner who finances a $20,000 solar installation will pay between $4,800 and $11,000 in interest over the life of their loan — a gap wide enough to wipe out years of electricity savings before a single panel pays for itself. The financing decision you make before signing anything is, in many cases, more consequential than the brand of panel you choose or the installer you hire. Two options dominate the conversation for homeowners with equity: the home equity line of credit (HELOC) and the dedicated solar loan. They look similar on paper, but they behave very differently in practice.

A HELOC lets you borrow against the equity you have already built in your home, typically at a variable interest rate that currently sits between 8% and 10% for well-qualified borrowers according to Federal Reserve consumer credit data. A solar loan is an unsecured or secured personal loan — often offered directly through your installer or a specialist lender like Mosaic or Sunlight Financial — with fixed rates that typically range from 5.99% to 14.99% depending on your credit score. Neither option is universally better. The right answer depends on your credit profile, how long you plan to stay in the home, your tax situation and your tolerance for rate risk.

This guide cuts through the marketing noise from both sides and gives you a clear framework for comparing the true cost of each path — including the tax angle that most solar financing articles overlook entirely.