The federal solar Investment Tax Credit (ITC) lets US homeowners cut 30% directly off their federal tax bill when they install a qualifying solar system — and in 2026 that credit is fully intact at its maximum rate. For the average residential system costing around $28,000 before incentives, that works out to an $8,400 reduction in what you owe the IRS. It is the single most valuable financial tool available to homeowners going solar, and yet IRS data consistently shows that eligible households either claim it incorrectly or fail to plan around it properly.

This guide covers everything you need to know about the 30% ITC in 2026: what exactly qualifies, how the credit interacts with your tax liability, which additional costs are covered beyond just the panels, and how to combine it with state-level incentives to drive your net cost even lower. The credit was extended and expanded under the Inflation Reduction Act of 2022, and under current law the 30% rate holds through 2032 before stepping down to 26% in 2033 and 22% in 2034.

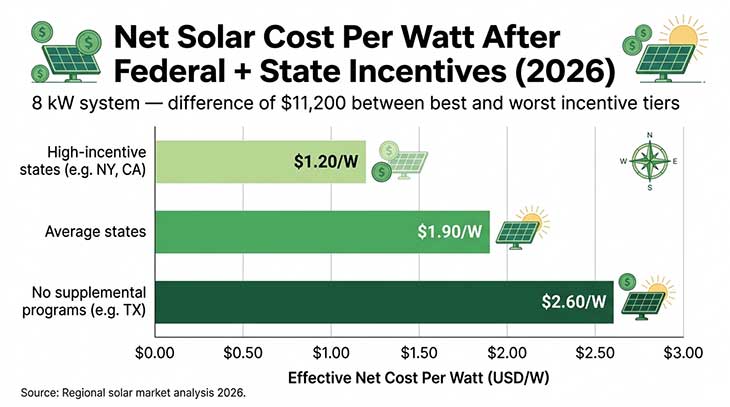

Understanding the numbers before you sign an installer contract is what separates homeowners who genuinely capture the full value of this incentive from those who leave money on the table. Use our solar tax credit calculator to run your own figures before reading the fine print below.